This is one of those questions that is hard to answer. One never knows what the future holds for us, but understanding your options can make all the difference in the world.

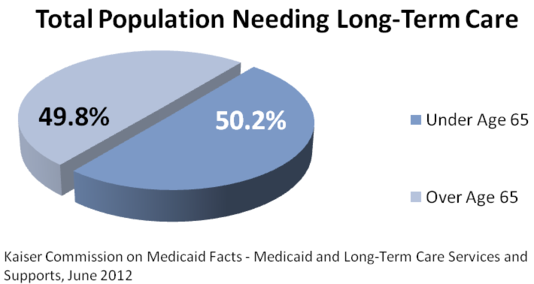

Most people believe that Long-term Care is something that only older people need, but that is not the case and the true numbers may surprise you. Longevity has been increasing over the years and with that fact, it is even more likely that people will need long term care in their lifetime.

- Between 2007 and 2015, the number of Americans ages 85 and older was expected to increase by 40 percent.

- By 2020, 12 million older Americans will need long term health care.

- By 2026, the population of Americans ages 65 and older will double to 71.5 million.

- Among people turning 65 today, 69 percent will need some form of long-term care, whether in the community or in a residential care facility.

These facilities can be very expensive and, depending on the type of care a person requires, can wipe out a person’s entire life savings within a very short period of time.

That is why it is so important that you understand your options and how this may impact you and your family’s future assets. There are different methods to protect your assets in case long term care is required, but it is up to you to determine which method is best for you.

Here are a few different methods that people use to fund their Long-Term Care.

- Self Insured – Meaning you are going to use 100% of your own assets to cover all incurred expenses. Self insuring for LTC is risky and can cost you your entire life savings. Remember that Medicare “does not” cover you for Long-Term Care!

- Medicaid – After you “spend down” most of your personal assets, the State will fund your Long-Term Care needs. Medicaid, unlike Medicare, will cover all your LTC needs, but you may not like the real price or the service. In order to qualify for Medicaid, you have to “spend down” your life savings to $10,000 and you get to keep your home and one car, but all future income will be turned over to the State to fund your LTC.

- Long-Term Care Insurance – Monthly premiums are paid to an insurance company for a specific benefit. Long-Term Care insurance can help pay for most of your LTC future needs, but it can be very expensive and who knows, maybe you will never use it. We find that talking to retirees about LTC insurance is like talking to a 20 year old about health insurance. Neither one of these people ever thinks that they’ll ever use it, but are grateful when it is needed. Plus, most policies only cover facility care and not home health care.

- Life Insurance – Life insurance with certain riders such as Accelerated Benefits Riders (ABR) or Long-term Care (LTC) riders can help fund some of these expenses. The one nice thing about this method is that it covers a few different options for care, but usually isn’t the best option for the price when you add-on a LTC rider. The ABR’s can be used to help and give you more options, but this is all based on how much life insurance you have in place with the right policy. For more information on this topic visit: https://safeguardassurance.com

- Annuity/LTC Combo – An Annuity that is designed to work as both an annuity and a Long-Term Care insurance policy. This option and its benefits will be explained below.

Of the methods listed above, they all have their pros and cons. As an example, your age at the time of purchase can make all the difference in what product approach is right for you. Life insurance has some major benefits, but depending on your age while adding a standard LTC rider, this may not be your best option.

But if you are looking for LTC funding while protecting what you have and getting the most bang for your buck, as financial professionals, we would recommend the Annuity/LTC combo option.

Annuities can be confusing and whether they are fixed or variable, they all work differently and you should always reevaluate your annuities on a regular basis. You should be aware of service charges, penalties, bonuses, caps, averages, point-to-point, capital gains, ERISA laws with Required Minimum Distribution (RMD), tax laws and the list goes on.

In regards to LTC, we like using the Annuity/LTC Combo as a vehicle to fund Long-Term Care. The reason is all the benefits it offers while protecting your assets.

Benefits include:

- 3 for 1 Long-Term Care benefits with No Out-of-Pocket Premiums(Example: $100,000 Annuity Provides $300,000 Long-Term Care Benefit)

- Money Back – Provides Long-Term Care benefits if you need them, or your annuity value, including net interest, if you don’t.

- Safety – Value is free from market risk.

- Liquidity – Interest can be accessed easily with no withdrawal charges.

- Long-Term Care Benefit – Reimbursed up to three times your annuity value for LTC benefits for six years or longer.

- Waiting Period – There is only a one-time 90-day deductible period.

- Tax Deferred Growth – Interest earned in your annuity accumulates tax deferred.

- Pre-Existing Conditions Are Covered – Benefits will not be denied for pre-existing conditions.

- Death Benefit – The full value of the annuity will be paid directly to the beneficiaries, bypassing probate.

- Tax Free – Withdrawals for Long-Term Care premiums and benefits are Tax Free!!!

Most annuities don’t offer these benefits so please contact us for more details. As you can see, if you have other annuities, savings or investments, this is a great way to fund your LTC needs while protecting your current and future assets.

As time goes on, we are living longer and things are becoming more expensive. Ask yourself this question: Do you think that health care will become cheaper or more expensive in the future?

Knowledge is power. Let us do a No Cost/No Obligation portfolio review while we evaluate financial options.